II. Macroeconomic Policies in time of COVID-19

MAINSTREAM AND ALTERNATIVES OF ECONOMIC POLICIES

Post 2

By. Juan M. Gutierrez

Using the pretext of the necessary budgetary austerity to be able to pay the public debt, governments and large multilateral institutions such as the World Bank, the IMF and regional banks such as the African Development Bank generalized a fiscal discipline that only pushed economies to use policies that deteriorated health systems. The precariousness of employment contracts, increased cost of medical care and medicines, reduction in investments in infrastructure and equipment, privatization of different sectors of health, reduction of public investment in research and development of treatments. We are in a historical moment that broken down into two acts, the first is the health crisis caused by the coronavirus and the second act is the recession accompanied by a stock market crisis and financial crisis. The financial crisis falls before the pandemic as well. The current financial crisis had all the elements of a new crisis that had been gathering elements for several years and that the coronavirus was the current trigger.

During the last week of February 2020, the worst week for the stock market since October 2008, major stock indices such as the Dow Jones fell 12.4%, the S&P 500 11.5% and the Nasdaq Composite 10, 5 %. Furthermore, it happened also in Europe and Asia, in the same days. The London Stock Exchange the FTSE-100 fell 11.32%, in Paris the CAC 40 12%, in Germany the DAX 12.44%, in the Tokyo Stock Exchange, the Nikkei fell 9.6%, the Chinese stocks (Shanghai, Shenzhen and Hong Kong) also fell. On Monday, March 2, due to the wave of massive interventions by central banks to sustain stock markets worldwide, the indices began to rise, except in London. On Tuesday the 3rd, the United States' FED panicked and reduced its prime rate by 0.50% (a decrease that can be considered as high). The new directing rate of the FED is now in a range of 1 to 1.25% and as the inflation rate in the United States between February 2019 and January 2020 reached 2.2%, in reality, the interest rate Actual Fed is negative. Despite the Fed's decision on Tuesday, March 3, the S&P index again fell 2.81% and the Dow Jones 2.9%. On March 3 and 4, several Asian exchanges also suffered a sharp decline. However, on March 4, there was a stock market surge in New York to celebrate Joe Biden's return to the presidential race.

What will happen in the stock markets in the coming days and weeks is unpredictable. However, it is crucial to analyze the plausible causes of the current financial crisis given that, as a global event, the economies and their international relations due to the products traded in Stock markets will affect the economies of nations. We focus our attention on the share price and the price of debt securities (also called obligations) that increased exaggeratedly concerning the evolution of production during the last ten years, accelerating in the last two or three years. The wealth of the wealthiest 1% also increased due to the direct relationship they have with the growth of financial assets. These large shareholders try to be the first to sell in order to obtain the best possible price before the price of these shares falls sharply. Significant investment funds, large banks, large industrial companies and billionaires order the sale of a part of the shares or titles of private debts (that is, obligations) that they own in order to pocket 15 or 20% of the rise in last years. It is said to be time to do it, and they call it collecting "profits."

These actions stripped of social awareness of the possible contagion effect on sales, the most important thing is to sell before the others; however, this can cause a domino effect and degenerate into a general crisis. They know this and console themselves by saying that they will come out pretty well as happened with a large number of billionaire shareholders in 2007-2009. On the other hand, there is an essential element that we must not neglect to observe that 1% of a thousand millionaires sells shares of private companies, which causes a drop in their prices and drags the drop in the stock markets, but at the same time they are buying securities of public debt considered as safe securities. As in the 2008 financial crisis, this is the case, mainly in the United States where the price of US Treasury securities increased due to strong demand. Let us notice that an increase in the price of the securities sold in the secondary market causes the performance to drop thereof. The wealthy who buy those Treasury Securities are willing to underperform since they are looking for security, at a time when the companies' share prices are declining. As a consequence, it must emphasize that once again, the titles of the states (national treasury bonds) are desirable to the richest because they consider them to be safer.

It is something not to forget since there are generally economic hoaxes about the public debt crisis and the market fears regarding government securities and their profitability or stability. The Big Capital considers that the rate of return that it obtains from the production is not sufficient then, it develops its financial activities independently of the production. However, this does not mean that it abandons production, but rather that it develops its investments to a greater extent in the financial sphere than in the productive sphere known as financialization, capital "makes profits" from fictitious capital through its highly speculative activities.

This development of the financial sphere increases the recourse to massive indebtedness of large companies (for more references see, Florian Gulli to Cedric Durand: "Fictitious capital, Cedric Durand", La Revue du projet; Michel Husson, "Marx et la finance : une approche actuelle", A l'Encontre, December 2001 .; Jean-Marie Harribey," La baudruche du capital fictif, lecture du Capital fictif de Cedric Durand ", Les Possibles, No. 6 - Printemps 2015 .; Francois Chesnais , "Capital fictif, dictature des actionnaires et des creanciers: enjeux du moment present" Les Possibles, N 6 - Printemps 2015.)

THE CHALLENGE OF ECONOMIC POLICYMAKERS IS MACROECONOMIC STABILITY.

Today is flooded by measures that brandish the old Keynesian systems driven mainly by government spending supported by debt measures. However, it is necessary to take into account the history of financial relations and the movement of the financial markets that had to do with financial crises supported by the so-called fiat money. Wealth cannot just go to one side of society since it produces significant asymmetries and decompensations of economic stability in crises created by toxic financial products.

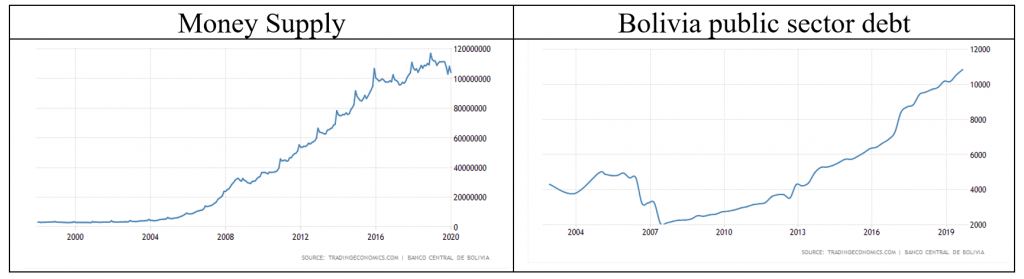

The effective policy for wealth redistribution cannot take money from one worker to give it to another, because the expense and level of income unbalanced by fiduciary money, so the debt does not create wealth or at least does not create it with the speed that compensates the effort of paying the debt. The classic example is the following: We returned to the previous report where it was writhen that the world as it is dollarized and will need dollars, it is the FED that will print those billions of dollars. However, the FED is not a governmental entity but a private entity that after printing the money when giving it to the American government, must pay some interest that the people would pay with taxes. There are reports that 3% of the money is physical, and 97% of the dollars are bits. According to the regulations in force in the USA, for every dollar deposited almost nine times its value they created by the fractional reserve banking system. Thus the current mainstream goes for the future creation of money to stabilize the commercial relations of the countries that require dollars to pay for transactions. However, if all central banks do the same as the FED, we would condemn the population to sink into less capacity payment and lower standards of living. The relationship that exists between the Money Supply of dollars vs purchasing power is the opposite.

OTHER MEASURES IN THE FACE OF THE CURRENT CRISIS

There are other measures such as the implementation of global tax reform with heavy taxation of capital, a global reduction in working time with compensatory contracts and the maintenance of the level of wages, free public health and educational services, of public transport, practical measures to guarantee equal pay. It is necessary to distribute wealth respecting social justice and privileging human rights and respect for fragile ecological balances. The vast majority of the population that sees their real incomes decrease or stagnate (real purchasing power) compensate for this decline or stagnation with the use of debt to maintain their level of consumption. Let us think vital questions: how to fill the fridge, ensuring the schooling of their children, how to get around to go to work, the necessary purchase of a car if there were no public transportation, how to pay the expenses generated by medical visits, etcetera, will only make the Bolivian economy more precarious and inequality gaps increase. It was necessary to provide radical solutions to prevent growing indebtedness and fall back policies individually cancellation family debts.

Therefore, a large part of families' private debts must cancel, primarily student debts, abusive mortgage debts, abusive consumer debts, debts linked to abusive microcredit, etcetera. The income of the majority of the population must increase, and the quality of public services, health, education, and corporate transportation must be sharply improved, all of which must be free. Support for the production of strategic sectors such as the production of Soy, Wheat, Sugar cane and quinoa is vital to be able to win markets that will be in dispute after the pandemic or any case in the new order of world economic relations.

Another Macroeconomics policy it is could also include Islamic Banking in the banking market, given the increase in its operations in the world under the following format. For example, Indonesia issued in 2003 a "fatwa" (Islamic decree) declaring bank interests an "illegal profit", the sector has only grown. Although the percentage of funds managed by Islamic banks is still minimal, the Government and the Bank of Indonesia look favourably on this trend and have taken steps in recent years to give the sector a boost. Islamic banks are not allowed to collect or pay interest, as Islam prohibits usury, nor can they finance projects related to gambling, firearms or alcohol. Profits and losses shared between the client and the bank. The basis of the business is similar to that of traditional banking: receiving deposits and making loans. However, the similarities end here. All the whys of that activity diverge enormously from the capitalist conception, resulting in a whole system regulated by religion. Nor should it be concluded that Islamic banking does not pursue profit. Like any other business or activity, it tries to maximize its benefits, only in this case, the limits of how it can and cannot obtain are more or less defined, since the only discussions given by different interpretations of the Islamic law whit relation to these issues. First, sharia prohibits charging interest - usury or riba - both for lenders and for those who deposit their money in the bank. Since Islam it is not conceived or approved that money in itself can create more money - the basic premise of modern banking operations - so that wealth can only come from productive activities and real work. Similarly, Islamic banks cannot invest or acquire financial elements that report interest, such as public debt. However, the ban on riba easily circumvented. Islamic Banking does not directly provide the money, acts as an intermediary between the loan applicant and the good or service for which the loan required.

Thus, both agree in advance on what management expenses the operation will carry - the item where the bank obtains the benefit - and how the customer will cover said payment. Once this resolved, the bank buys the good or service that the customer wants and later sells it to them in instalments for the agreed amount. In the case of businesses or companies, the peculiarities are also numerous. Both the entrepreneur and the entity will share profits or losses in an investment. Under the precepts of Islamic law, unable to collect interest, banks finance a part of the investment, matched with the benefits of the company in the same proportion as its financing. Over time the entrepreneur will be able to buy the part of the company that corresponds to the bank. Meanwhile, the entity pays for its investment with dividends. Logically this company can only engage in an activity that produces real wealth through work. In the proposed summary:

- Prohibition of interest rates as such ("riba"), although it does allow charging a margin in operation;

- Prohibition on transactions in which there is uncertainty ("gharar") ambiguity ("jahala") in a way that leaves out financial derivatives (forward, options and futures, and hedge funds);

- Prohibition of illegal activities ("haram") that go against the moral and religious principles of Sharee'ah (investments in drugs, alcohol or pork products, arms smuggling, gambling, immoral film industry).

- The purpose of the activity financed by Islamic Banking should not harm society or individuals.

Numero Basico de Reproduccion de Epidemias R0 COVID-19 para Bolivia

Es justo decir que el perfil de riesgo de la crisis de Covid-19 es particularmente amenazante. Si bien existe un libro de jugadas de politicas economicas para hacer frente a las crisis financieras, no existe tal cosa para una congelacion de la economia real a gran escala.

Macroeconomic Policies in time of COVID-19

The COVID-19 pandemic has generated an unprecedented economic crisis. The leading global economies are in a sharp recession, and this will inevitably impact Latin America.

¿Necesitas resolver algo parecido?

Modelización cuantitativa, validación de modelos y data leadership. Trabajo bajo NDA si lo pides.

Háblame de tu proyecto →